B2B OTT Ecosystem: How Telcos Can Launch Faster, Spend Smarter, and Compete on UX

Quick Summary

The conversation around OTT has changed: it’s no longer just about launching a streaming app, but about how operators can build a sustainable streaming business that is fast, at scale, and without turning every feature into a bespoke engineering project. That was the underlying theme of the panel “A1 and UniqCast: B2B OTT Ecosystem for Telcos,” hosted by NEM Zagreb. This session was an operator-focused discussion, featuring key speakers Elena Petrova, A1 and Darko Robič, UniqCast, that surfaced some of the most practical lessons about what it takes to compete in today’s video market.

This article is inspired by that session, but it deliberately broadens the lens. Because the challenge isn’t unique to any single telco or vendor. Regional operators, ISPs, and content providers are under pressure to deliver premium multiscreen UX and strong content from day one, yet they’re still blocked by the same two friction points: high upfront investment and long time-to-market. The result is a growing demand for a new model: a B2B OTT Ecosystem approach where content, technology, operations, and scalability are designed as one repeatable product, not assembled from scratch for every launch.

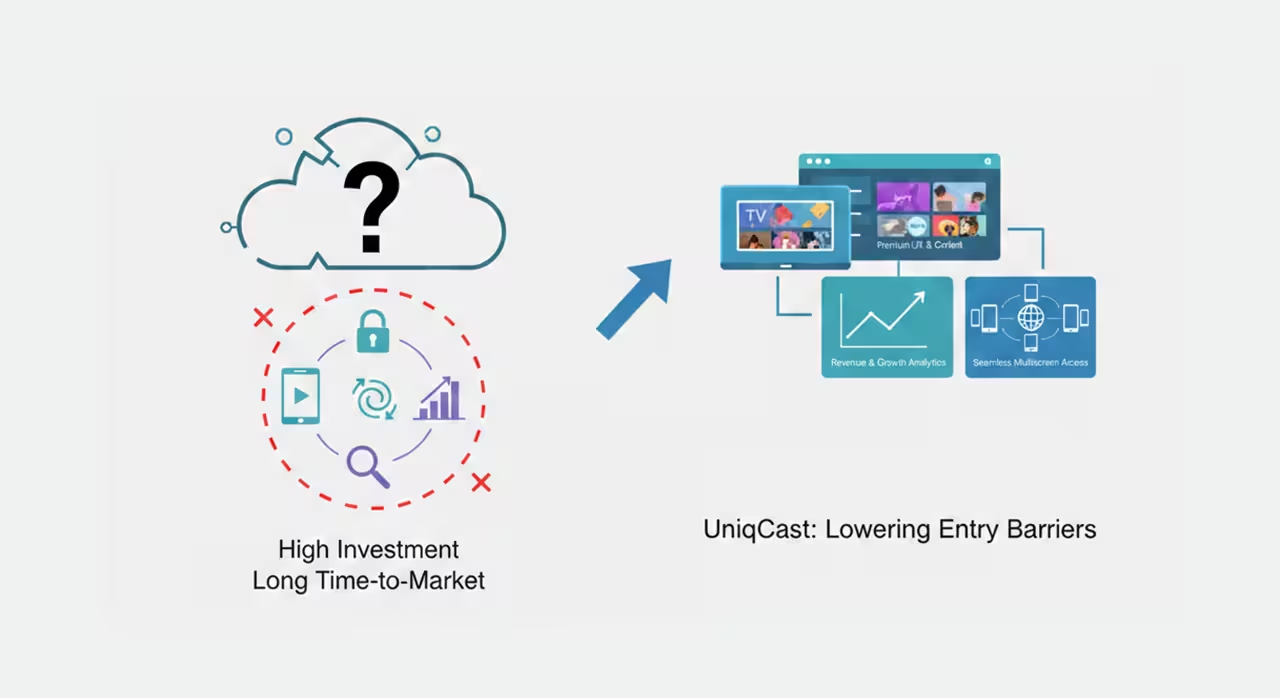

The market gap: Everyone needs OTT, but not everyone can build it

Viewers now expect the same things from their telco TV service that they get from global streamers: a premium, intuitive UX, seamless multiscreen access, and a content proposition that feels complete from day one. And that expectation hits every market segment: regional telcos, ISPs bundling TV to reduce churn, and content providers looking for new routes to audiences.

On the other hand, many telcos want to offer a modern OTT service, yet they run into two recurring blockers: high upfront investment and long time-to-market with traditional deployments. In practice, those aren’t just financial and scheduling headaches; they’re structural barriers that can stop a project before it even starts.

Why?

Because building an OTT platform is a chain of decisions and ongoing responsibilities. Even a seemingly straightforward launch can quickly expand into:

- multi-device apps and ongoing device certification cycles,

- content security (DRM), entitlement, and subscriber management,

- streaming infrastructure and performance engineering,

- metadata, search, recommendations, and discovery UX,

- analytics, operations, and customer support workflows.

The result is a market gap that’s become increasingly visible: operators want to deliver streaming-grade TV, but many cannot justify (or staff) a multi-year platform build before they’ve proven adoption and revenue. That gap is exactly where the B2B OTT Ecosystem approach is gaining momentum. With it, we’re moving from custom, one-off OTT projects to repeatable, scalable services designed to lower entry barriers while still meeting modern UX and content expectations.

Why ecosystems win: integrating content + technology

One of the most common reasons OTT projects stall is fragmentation. Operators often end up “assembling” their service from a patchwork of components: one vendor for apps, another for CMS, another for CDN, another for DRM, another for analytics, plus separate content deals and distribution workflows layered on top. On paper, that sounds flexible. In reality, it frequently creates vendor sprawl: longer integrations, slower launches, unclear accountability when something breaks, and a roadmap that’s hard to steer because every change ripples across multiple suppliers.

That’s why the ecosystem approach is increasingly compelling: it treats OTT less like a DIY tech stack and more like an operator-ready product where content, technology, and operations are designed to work together from the start. Many white-label offerings still lean heavily in one direction (either content or technology) while very few combine both in a way that is “operationally seamless for the operator.” The practical advantage is straightforward: when content delivery workflows and platform capabilities are already aligned, an operator can focus on service design (packaging, positioning, differentiation) instead of spending months coordinating vendors and solving integration edge cases.

The A1–UniqCast partnership discussed during the panel is useful here as an example, because it clearly illustrates what “ecosystem” means in practice: content plus an end-to-end platform delivered as one integrated service, not fragmented pieces. This includes both the content foundation (rights-cleared channels, distribution readiness) and the full technical stack required for multiscreen delivery: apps, CMS, transcoding, DRM, analytics, and more, so operators don’t have to stitch these parts together themselves.

“Simplicity, speed, scalability, low upfront investment, pay as you grow model and being close to our customers – on the content side, on the technical side and on the support side. “, Elena Petrova, A1 on the question about how partnership with UniqCast creates a competitive advantage compared to other white-label OTT solutions.

Operators highly value speed, but also the assurance of a structured onboarding process and a unified support model, because it reduces the “multi-vendor ping-pong” that slows troubleshooting and decision-making. When operators feel they’re getting a complete solution rather than managing multiple suppliers, they can move faster internally, launch with more confidence, and iterate without renegotiating the entire stack every time they want to improve the service.

Multi-tenant cloud as the real enabler

It’s easy to hear “cloud” and assume the conversation is mainly about infrastructure, where servers run, how elastic capacity is, or whether a platform is hosted or on-prem. But in B2B OTT, multi-tenant cloud is less about hosting and more about how the business scales. It’s the difference between building a separate platform for every operator and delivering a shared core that can be configured, branded, and operated across many operators without duplicating effort.

For platforms like UniqCast, multi-tenancy comes through as a foundational design principle: a shared cloud platform that supports multiple operators (and potentially multiple services per operator) while still allowing each “tenant” to have its own commercial rules, user experience, and content offer. That matters because the promise of a B2B OTT ecosystem (fast launches and pay-as-you-grow economics) only works if the underlying technology can deliver repeatability without forcing everyone into the same cookie-cutter service.

A properly implemented multi-tenant model typically enables three things operators care about immediately:

1) Faster launches through configuration, not custom development

Instead of starting from scratch for each new market or partner, operators can spin up a tenant and configure the service: branding, navigation structure, homepage rails, packages, language settings, entitlement rules, and even device rollouts without a long rebuild cycle. This is where time-to-market improves in a way that’s structural, not just project management efficiency.

2) Scale economics without sacrificing differentiation

Multi-tenant architecture makes it possible to share the heavy lifting (core services, updates, performance improvements, and operational tooling) across multiple deployments, while still keeping the service-level identity distinct. Operators get economies of scale, but they don’t have to give up the ability to localize and differentiate.

3) A smoother path through compliance and operational variance

Operators face diverse regulatory and commercial environments. This market variability, including compliance requirements and differing ways services must be packaged, managed, or reported, is effectively managed by multi-tenancy. Instead of requiring customized product versions (bespoke forks), multi-tenancy accommodates these differences through tenant-level configuration and policy controls within a single platform.

This is also why multi-tenancy shouldn’t be treated as a checkbox claim. Many platforms can be hosted in the cloud; fewer are genuinely designed for multi-operator scale. The practical questions operators should ask (and vendors should be ready to answer) include: how tenant isolation is enforced (data, entitlements, analytics), how releases are rolled out without breaking custom configurations, and how quickly a new tenant can be launched without engineering work. Those details determine whether cloud is simply a deployment model or the engine that makes an ecosystem commercially viable.

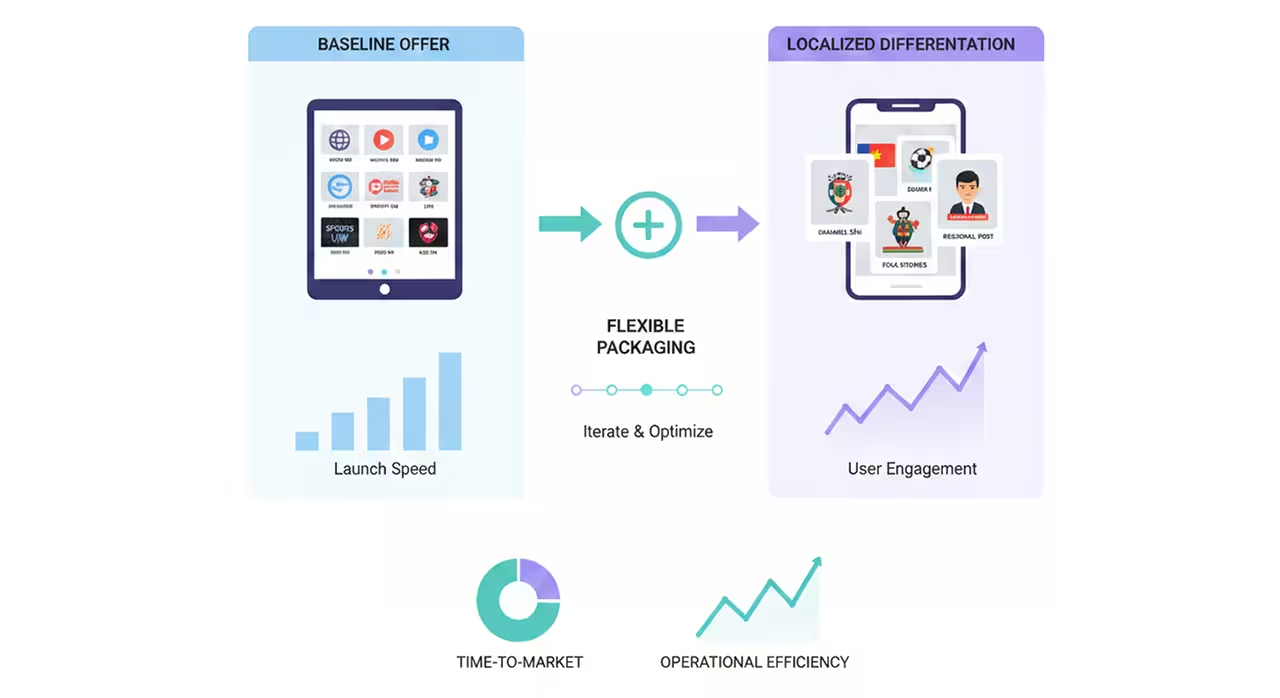

Content strategy: start with a strong baseline, then localize to win

For telcos, content strategy is often where OTT ambitions meet reality. A platform can be technically excellent, but if the service launches with a thin offer or an offer that doesn’t match local viewing habits users won’t stick around long enough to discover the UX improvements. That’s why the “ecosystem” approach doesn’t treat content as something bolted on after the platform is delivered. Instead, content becomes part of the go-to-market foundation: a strong baseline offer that makes the service viable at launch, with a clear path to local differentiation.

In the panel discussion, this logic is explicit: operators want to launch quickly, and that’s much easier when there is a “ready-to-launch” content proposition available. Especially for smaller telcos and ISPs that may not have the leverage, team size, or time to negotiate dozens of separate deals. A strong baseline offer with popular channels, familiar genres, a coherent package structure helps the operator clear the first hurdle: being perceived as a credible TV destination from day one.

But the baseline isn’t what wins the long game. Localization is. Operators still need the ability to tailor the content mix to local market expectations, thus adding national channels, local broadcasters, regional sports, culturally relevant programming, and niche content that global packages don’t cover well. This is where many OTT launches either gain momentum or plateau: if the service feels generic, it risks becoming interchangeable with other offers; if it feels locally curated, it becomes part of a household routine.

A practical content playbook emerges from this “baseline + localization” model:

- Launch with a complete starter package that reduces time-to-market and avoids the perception of a “beta” service.

- Differentiate with local value quickly, prioritizing the channels and content categories that are habitual and culturally anchored in the market.

- Keep packaging flexible so operators can iterate: seasonal offers, trial bundles, sports add-ons, and targeted niche packs without rebuilding the service each time.

Importantly, localization isn’t only about acquiring content. It’s also about the platform’s ability to manage localized content efficiently: rapid metadata updates, clear rights handling (including catch-up rules), EPG accuracy, and the operational workflows needed to keep live TV and VOD aligned across devices. If those workflows are slow or manual, localization becomes expensive and brittle; if they’re optimized, localization becomes the operator’s competitive advantage.

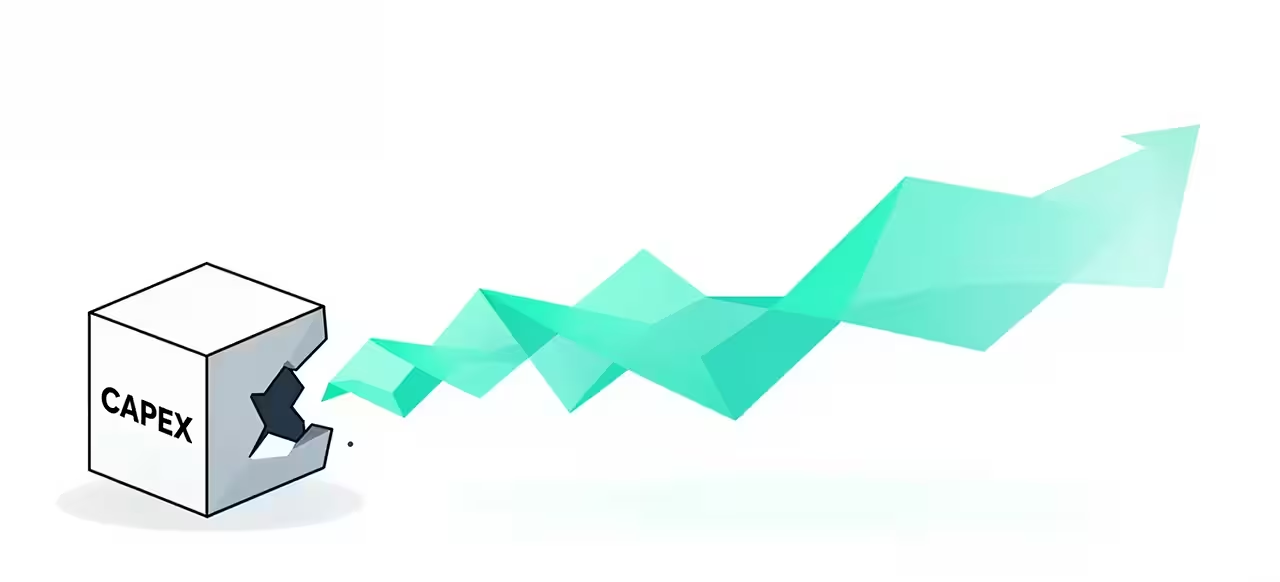

The business model shift: from CAPEX to pay-as-you-grow systems

For years, many operator video projects followed the same financial logic: buy (or build) a platform, invest heavily upfront, run a long integration and device rollout cycle, and only then start measuring whether the service is gaining traction. That model is increasingly hard to justify, not because OTT isn’t strategic, but because the market has become too fluid. Consumer expectations shift quickly, competitors move faster, and content economics can change mid-project. In that environment, tying OTT to a large CAPEX commitment before the first subscriber even logs in is a risky bet.

That’s why the “ecosystem” model points to a clear economic shift: moving away from CAPEX-heavy builds toward pay-as-you-grow scaling, where costs align more directly with adoption. In practical terms, this means operators can launch with a predictable operational cost base and expand capacity, functionality, and content investment as the user base grows, rather than trying to forecast everything upfront and overbuilding “just in case.”

This shift matters most for two groups that often sit outside the spotlight in OTT conversations:

1) Smaller operators and ISPs.

These players often know that in OTT it is necessary to reduce churn and remain competitive, but they don’t always have the budget or specialist teams to fund and manage a large, custom deployment. Lowering entry barriers (financial and operational) is a key driver for B2B OTT adoption in these segments. Pay-as-you-grow models allow them to launch credibly, learn what their market responds to, and iterate without staking the business case on a “big bang” transformation.

2) Emerging markets and growth markets.

In many regions, the opportunity is real, but so are the constraints: procurement cycles can be longer, internal platform engineering resources are limited, and the addressable market may be growing unevenly. Flexible economics help operators match investment to reality rather than to optimistic projections.

Beyond affordability, pay-as-you-grow changes the tempo of product decision-making. When an operator isn’t locked into sunk costs and multi-year platform depreciation logic, it becomes easier to experiment with:

- packaging and bundle structures,

- new content add-ons (sports, kids, local niches),

- device expansion strategies,

- hybrid monetization options over time.

It also reduces project risk in a very direct way: if adoption is slower than expected, the business impact is contained; if adoption is faster, scaling is operationally and financially smoother. And because ecosystem models typically share core platform operations across multiple tenants, upgrades and improvements don’t require “re-buying” the platform each time the market shifts, they’re part of an ongoing service evolution.

Premium UX: The Bare Minimum for Churn Control and Competitiveness

In operator video, UX has become a business lever, because in a world of abundant choice, the easiest service to use is often the one people keep. That’s why many telcos now treat premium UX as the competitive minimum: not a differentiator on its own, but a prerequisite for reducing churn and protecting the value of broadband and bundle relationships.

Modern platforms, such as UniqCast, reflect this shift by repeatedly anchoring the OTT value proposition in practical user-facing outcomes: modern multiscreen access, consistent experiences across devices, and service usability that matches what consumers have learned from global streaming brands. What’s important is the implication behind that: if your service feels slower, harder to navigate, or less coherent than the alternatives, users won’t necessarily complain, but they’ll simply stop opening it, and the operator loses engagement that should have reinforced loyalty.

In practice, premium UX isn’t one feature. It’s a set of capabilities that together reduce friction in everyday viewing:

Consistency across devices (true multiscreen).

Users don’t think in platforms, but they think in moments. They start watching on one screen, continue on another, and expect watchlists, favorites, and navigation patterns to follow them. Multiscreen is therefore not just apps everywhere, but a coherent experience that feels like one service regardless of device.

Fast performance where it matters.

For live TV especially, the UX is defined by responsiveness: channel change speed, quick start time, stable playback, and smooth transitions. If performance lags, the interface can look modern but still feel frustrating in real use, particularly for households that compare it directly with established TV habits.

Discovery that helps viewers decide, not just browse.

A vast catalog doesn't inherently translate to a superior service if users struggle to locate desired content. Discovery stands as a crucial value proposition, embodied by concepts like "Discover and Watch." This design philosophy aims to improve the user experience, rapidly transitioning users from intent to playback, thereby reducing the classic “choice overload” problem.

The churn-control argument becomes even stronger when you look at how operators actually compete. Many telcos are not trying to outspend global players on exclusive content; they’re competing on service convenience, bundle value, and daily reliability. In that context, a modern, intuitive UX is the element that makes the whole proposition feel worth keeping, even when users also subscribe to one or more global streamers.

And this is where the ecosystem model links back to execution reality. Building “great UX” as a one-off project is possible, but it’s hard to sustain, because UX expectations evolve quickly, device platforms update constantly, and consumer reference points keep rising. A B2B OTT ecosystem approach makes UX improvement more continuous: operators benefit from platform-level enhancements (performance, UI capabilities, discovery features) while still controlling how the experience is presented to their own users.

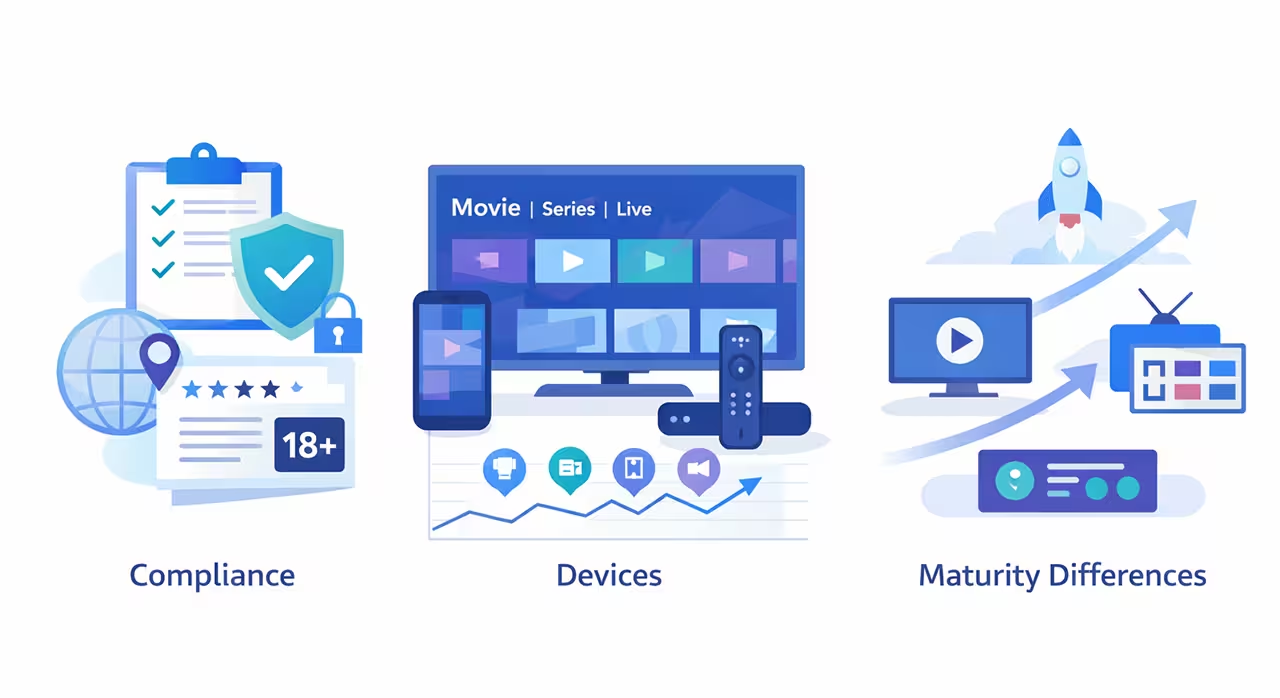

International reality: compliance, devices, and maturity differences

If OTT were only about building one great product, scaling internationally would be straightforward: repeat the same launch plan market after market. In reality, cross-market deployment is where many “perfect on paper” strategies hit friction, because operators differ by regulation, device ecosystems, and the maturity of the platforms they’re replacing. Any B2B OTT model that claims to be repeatable has to prove it can absorb those differences without collapsing into custom projects again.

Compliance is a market-by-market operating condition

Regulatory and contractual requirements vary widely: privacy and data handling rules, content ratings and age restrictions, catch-up permissions, recording rules, and rights windows can all change depending on territory and content type. The key point isn’t simply “be compliant”. It’s that compliance needs to be manageable. If every regional rule creates a new code branch or custom integration, scalability disappears. Multi-tenant approaches work best when these differences can be handled through policy controls and configuration (where possible), with clear operational governance around what can be adjusted per tenant.

Device reality: certification and maintenance are ongoing work

Operators also face a device landscape that is messier than many outsiders assume. There’s the obvious range: STBs, smart TVs, mobile devices, browsers, but also the long tail of OS versions, chipset differences, DRM support, and platform certification requirements. What matters operationally is that device support is a continuous commitment: updates, regressions, app store changes, OEM firmware updates, and new device launches all create ongoing work. A scalable approach requires tooling and processes that make device maintenance predictable, especially if multiple operators are served from the same platform foundation.

Maturity differences: not everyone is starting OTT from the same place

Finally, operators come into OTT with very different starting points. Some are launching OTT-first; others are migrating from legacy IPTV stacks; others are somewhere in between, running hybrid operations while modernizing. The practical implication is that a “one-size-fits-all” rollout path usually fails. A mature B2B OTT ecosystem needs to support multiple adoption paths:

- OTT-first launches that prioritize speed and device reach

- Legacy replacement programs that prioritize migration, service continuity, and operational stability

- Hybrid strategies that let operators evolve without disruption

This is why international scale is less about finding a universal product configuration and more about building a platform and operations model that can absorb real-world variations.

Early deployment lessons: speed is the headline, onboarding is the differentiator

When operators talk about launching OTT, the conversation often starts with speed and for good reason. Time-to-market determines whether an operator can respond to competition, meet internal targets, and start learning from real usage instead of assumptions. But early deployments reveal a more nuanced truth: speed gets attention, while onboarding determines whether scale is actually achievable.

As the panel reflects, the real operational value of the B2B OTT ecosystem emerges from what happens immediately after launch: how quickly a new operator (or a new market rollout) can be set up, trained, supported, and moved into stable operation. In a multi-tenant ecosystem model, onboarding is the mechanism that turns a platform into a productized service.

Lesson 1: Launch speed matters, but repeatability matters more

A fast first rollout can still be a dead end if every next rollout requires the same heavy involvement from senior engineers and “heroic” project work. Early deployments highlight the need for a standardized onboarding track: tenant setup, configuration templates, packaging workflows, operational playbooks, and a clear division of responsibilities. The goal is to make “go live” a predictable motion.

Lesson 2: Simplicity is a feature (especially for legacy replacements)

Operators migrating from older TV stacks are often dealing with internal complexity: legacy processes, established customer support scripts, device fleets, and existing subscriber entitlements. In that context, onboarding is most successful when the ecosystem reduces moving parts: fewer vendors, fewer handovers, clearer accountability, and a platform that can be configured without constant custom development. This is where the ecosystem model becomes practical.

Lesson 3: Content and service packaging must be flexible from day one

Early rollout experience also reinforces that operators rarely “get it perfect” at launch and they shouldn’t have to. Operators learn quickly which packs convert, which channels drive daily engagement, what kinds of VOD matter locally, and which UX pathways create drop-off. The platform and operations model needs to support this learning loop: easy packaging adjustments, metadata updates, and controlled changes without destabilizing the service.

Lesson 4: Unified support reduces friction and accelerates improvement

In multi-vendor setups, troubleshooting often becomes a coordination problem: every issue risks turning into a blame loop between suppliers. Early deployments highlight the opposite advantage of the ecosystem approach: when content and technology are integrated under a coordinated service model, operators get clearer escalation paths and faster resolution. That directly affects the speed of iteration, because it’s hard to improve UX or add capabilities if the operational model can’t respond quickly to real-world issues.

The takeaway from early deployment is simple: speed is the headline operators want, but onboarding is what makes the headline repeatable. A B2B OTT ecosystem wins when it combines fast launches with a disciplined onboarding and support model.

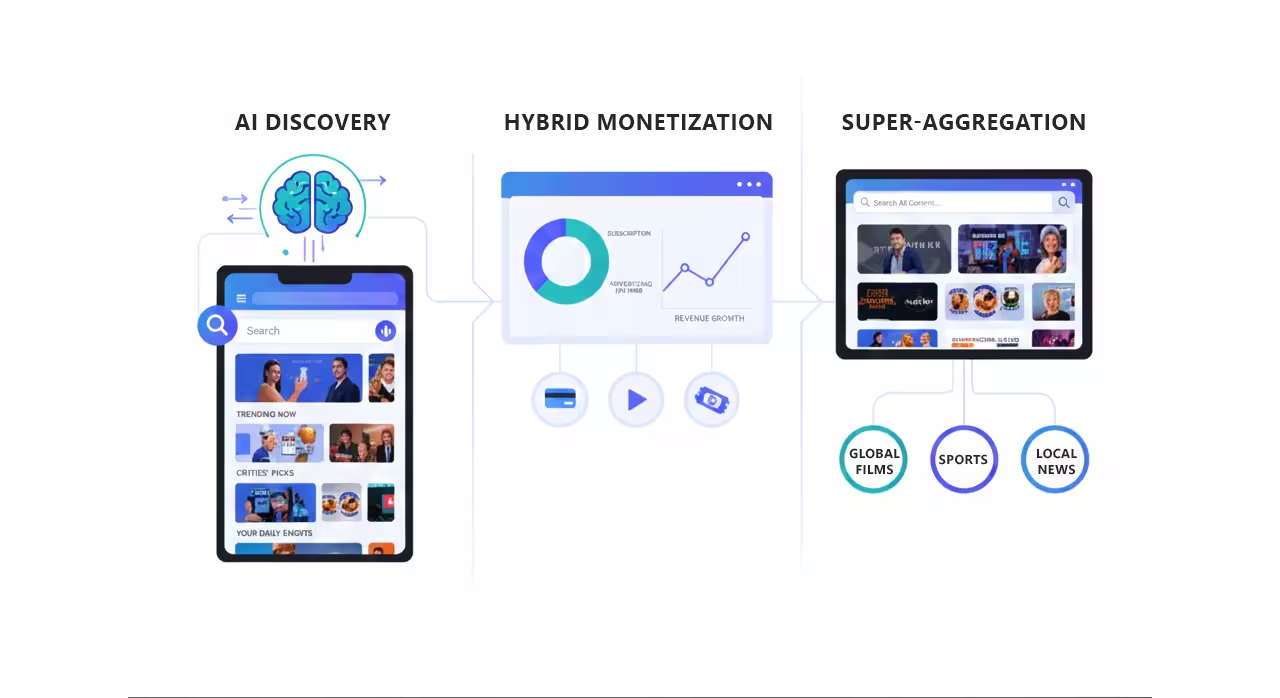

Where it’s going next: AI discovery, hybrid monetization, and super-aggregation

If the last few years of operator OTT were defined by “getting the service live” (apps, devices, core streaming quality), the next phase is about making the service smarter, more monetizable, and less fragmented, without turning every improvement into a heavyweight integration project. The future of OTT points to three trajectories that are quickly becoming interconnected: AI-driven discovery, hybrid monetization, and super-aggregation.

AI discovery moves beyond “recommended for you”

Classic personalization is table stakes. What’s changing is how discovery happens and how directly it drives viewing decisions. Instead of relying only on static rails or generic recommendation rows, AI is increasingly used to keep the catalogue “alive” and context-aware, thus reshaping the home experience based on what’s trending, what’s new, and what different audience segments are responding to.

The panel highlights several directions that represent this shift from passive discovery to guided viewing:

- Dynamic catalogues that automatically reorganize live TV, catch-up, and VOD into thematic rails using signals like genre, cast, release date, and popularity trends, so the service stays fresh without manual curation becoming a bottleneck.

- Voice-assisted navigation to shorten the distance between intent and playback, especially on TV screens where typing is friction.

- Scene-level search that lets users jump to specific moments inside a show, which is a meaningful UX upgrade beyond searching content by its title.

- AI-generated shorts (vertical, bite-sized previews) that act as discovery teasers for long-form content, helping users decide what to watch faster and helping operators increase visibility and conversion for content that might otherwise be buried.

“Today we’re not searching only through metadata of content, but we are analyzing and understanding the (context of) the content itself. The result is obvious, users engage more, they stay with the service more and it provides a fun and dynamic way of interacting with content.”, Darko Robič, UniqCast, on the question of how UniqCast is using AI today to create smarter, more efficient, and more engaging experiences for operators and their customers.

Hybrid monetization becomes the default, not the exception

Here is a commercial reality that operators are leaning into: pure subscription models don’t always maximize revenue, and pure ad models aren’t always sufficient for premium content. So operators increasingly explore hybrid approaches t.i. subscription combined with advertising, and/or transactional VOD layers for specific titles, events, or windows.

For operators, this matters because monetization flexibility enables better packaging strategy: different tiers, different ad loads, promotions tied to audience segments, and market-specific offers, all without rebuilding the service.

Super-aggregation: solving fragmentation with one coherent UX

Finally, super-aggregation is the structural answer to a problem every operator hears from customers: “I don’t know where to watch this.” Instead of forcing users to hop between separate apps and disconnected catalogs, the direction described is to unify third-party catalogues, local broadcasters, niche VOD providers, and even standalone streaming apps into a single, coherent UX.

The mechanics matter here: super-aggregation means integrating external sources by ingesting metadata and merging them into dynamic, discoverable rails, so users browse “one service” rather than a collection of separate destinations.

Taken together, these three trends point to the same end-state: OTT services that are easier to navigate, easier to monetize, and easier to expand. The winners will be those who make complexity invisible to the user while giving operators more intelligence and flexibility behind the scenes.

Conclusion: a decision framework for telcos

The core message behind the B2B OTT Ecosystem idea is simple: telcos don’t need another platform project, they need a repeatable way to launch, operate, and evolve video services at market speed. The panel discussion underlines why this matters now: operators are squeezed between rising user expectations (streaming-grade multiscreen UX, strong discovery, consistent performance) and the practical constraints that slow traditional OTT deployments with upfront cost, long integration cycles, and operational complexity.

For decision-makers, the takeaway is not “choose an ecosystem because it’s trendy,” but use a clear framework to evaluate whether an ecosystem model will actually deliver speed and control. Here’s a practical checklist to guide vendor and partner evaluation:

- Multi-tenancy depth (not just cloud hosting): Can you launch and run distinct services through configuration, with proper tenant isolation for users, entitlements, analytics, and data?

- Time-to-market and onboarding: How quickly can a new tenant go live and what does the onboarding playbook look like for training, operations, and ongoing support?

- Content flexibility and localization: Can you start with a baseline offer and still localize fast: channels, rights rules, packaging, metadata, and catch-up policies, without constant reintegration?

- Device coverage and lifecycle readiness: Does the solution support the device reality you operate in today and does it include the processes to maintain and evolve apps across device ecosystems?

- UX and discovery maturity: Does the service deliver consistent multiscreen UX and discovery that helps users decide quickly (not just browse), with a clear roadmap toward AI-led discovery improvements?

- Monetization readiness: Can you support hybrid models over time: subscription, ads (including DAI/targeting), and transactional layers without re-architecting the service?

- Roadmap credibility toward super-aggregation: Can the platform unify third-party catalogues and services into one UX so your offer becomes simpler, not more fragmented, as you add partners?

A well-executed B2B OTT Ecosystem can reduce friction (financially, technically, and operationally), while still leaving operators room to differentiate through local content, packaging, and experience. The real decision is whether the model you choose lets you compete and evolve continuously, instead of rebuilding the same stack every time the market changes.